We might see banks and other financial institutions as a means to help us. They keep our money safe, invest to give profits, their credit and debit cards give us ease of spending and much more. What most people do forget is that these institutions are, like all and any other business, operating to make profits for themselves.

The main earning of these institutions is through interest and returns on investments. When it comes to handing out loans, they will always look out for their interests first. Any application is scrutinized carefully, with plans and feasibility reports on how much return they would get for their investments. Big companies looking for loans or credit lines can get finances relatively easily. Their performance and the huge amount they need is sufficient enough for banks and other capital investment companies to give their required amount.

Small Fish In Big Seas

Small and Medium Enterprises (SMEs) are considered the backbone of emerging markets. They account for nearly 95% of businesses worldwide and employ 65% of the global workforce. An estimated 600 million jobs will be created in the next 15 years by SMEs, making this a very lucrative market.

Yet, a crucial issue exists. With a monetary gap of over 1.2 trillion dollars, the SME sector has a hard time getting loans and credits. There are a number of reasons.

- Pledge: SMEs have little assets to offer a guarantee for the level of investment they seek.

- Risky Market: Although the gains in investments are very high, the volatile nature of the market creates a risk that normally banks and financial institutions avoid.

- Low Return: The small amounts of loans required make it unfeasible to even hand it out.

- Credit History: Since SMEs mostly rely on cash, the credit history is not built enough to convince institutions to give loans.

- Lack of Information: Most SMEs lack proper paperwork that would put their information and financial management in proper format for banks. The uncertainty in the paperwork means capital investors would not even consider lending money.

- Prohibitive Terms: The high risks mean that the borrowing costs are too much for SMEs to seek out loans.

- Trust: With little to back up, the banks and institutions are wary and avoid investing.

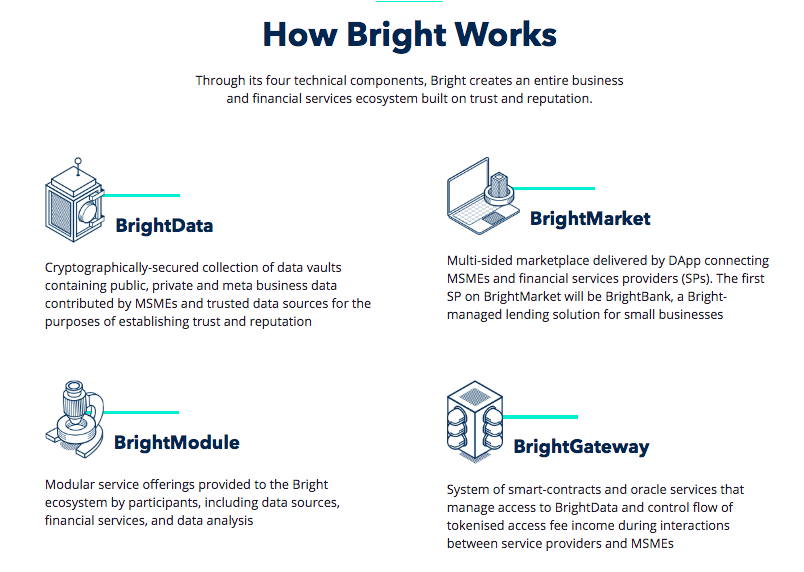

Bright’s Decentralized Loans

Bright is a blockchain based institution that understands the needs of SMEs and the apparent issues in securing loans and money these companies and businesses face. In order to fill the 1.2 trillion dollar gap, the platform has created a decentralized network which is specifically designed to cater for SMEs and their unique credit and loan requirements.

Pierre Proner, CEO of Bright says that the platform’s mission is “to address the issues MSMEs face, head on. Small businesses in emerging markets experience limited access to finance, and thus face difficulty growing their businesses. By leveraging blockchain technology and data science, we are able to provide small businesses with loans and begin to close the credit gap that prevents them from becoming greater participants in the global economy.”

The Bright’s platform allows for peer to peer lending, creating a whole new lending economy that will be powered by users themselves. The platform allows:

- Unsecured Lending: By using blockchain, data is transparent and lenders are at more ease, allowing for more borrower-friendly plans and competitive terms.

- Secured Lending: Collateral lenders are more accurate in predicting default rates, offering better pledging and pricing terms.

- KYC And AML Checks: With other users rating SMEs, this will create a Know Your Customer and Anti Money Laundering check that would otherwise not pass the rigid protocols of banks.

- Credit Checks: A more accurate scenario of SMEs credit will be developed, leading to easier and larger loans over time.

- References: Businesses can recommend and rate other SMEs, building a reference and reputation rating that will bring down borrower costs of securing loans.

- Monetization of Data: Market researchers can ask for business data from SMEs and pay them, creating another line of monetary input for the small fledgling businesses.

Third Party Financial Services

Over a period of time, as the Bright network grows and matures, it will attract the attention of traditional lending firms and they would be eager to tap into the vast market full of potential. The Bright platform will open itself up when the time is right, allowing for more influx of money and thereby creating a larger opportunity pool for SMEs to secure loans.

By creating a platform for Small and Medium Enterprises to secure loans, the Bright platform will fill a multibillion-dollar gap in the industry and bring liquidity to thousands of businesses around the world. Creating a pull factor, it will bring in more and more money investing organizations and create an ecosystem that will cater to the largest business sector in the world.

Visit the website for more information https://brightnetwork.io/